If the last few years have taught us anything in the world of real estate and finance, it is that preparation is power. As we look toward the horizon of 2026, homeowners and prospective buyers in Kitchener-Waterloo face a unique economic landscape. Whether you are looking to purchase your first home, renewing a mortgage that was locked in during the low-rate era, or considering leveraging equity for investment, having a strategic plan is non-negotiable.

At Mortgage Architects Bennett Capital Group, we believe that your mortgage should work for you, not the other way around. Led by Tracy Bennett, a veteran mortgage planner with over 35 years of experience, our team creates personalized roadmaps that account for market shifts, interest rate forecasts, and your personal financial goals. Here is your comprehensive guide to mortgage planning for 2026.

The year 2026 is shaping up to be a significant milestone for the Canadian housing market. Many mortgages originated during the peak of the housing boom (2020-2021) will be coming up for renewal. For many residents in the Waterloo Region, this means transitioning from historically low interest rates to a new financial reality.

However, it isn't all challenges. Markets are cyclical. By planning now, you can mitigate "payment shock," take advantage of potential rate stabilizations, and position yourself to build wealth. A proactive approach involves reviewing your current financial health, understanding the local Kitchener real estate market, and consulting with a trusted mortgage broker well before your maturity date.

Real estate is hyper-local. While national headlines give a broad overview, the dynamics in Kitchener, Waterloo, and Cambridge are distinct. Our region remains a hub for technology, education, and manufacturing, driving consistent demand for housing.

Inventory Levels: We anticipate a balanced market in 2026, offering more negotiation power for buyers than in previous frenzied years.

Population Growth: With new Canadians and young professionals moving to the Tri-Cities, competition for entry-level homes and rentals remains steady.

Property Values: While prices have stabilized, long-term equity growth in Kitchener remains a strong bet for wealth accumulation.

Whether you are looking at a condo in downtown Kitchener or a detached home in the suburbs, understanding these local nuances is part of our service at Bennett Capital Group from Mortgage Architects. We don't just find you a rate; we help you find a home strategy.

One size does not fit all. Your roadmap for 2026 depends entirely on your current position on the property ladder.

1. The Roadmap for First-Time Home Buyers

If 2026 is the year you plan to stop renting and start owning, you need to start preparing 6 to 12 months in advance. The "dream of homeownership" requires concrete financial steps.

Credit Consulting: A strong credit score is your ticket to the best rates. We offer credit consulting to help you polish your report before lenders see it.

Down Payment Strategy: Are you utilizing the First Home Savings Account (FHSA) or the Home Buyers' Plan (HBP)? We can guide you on how to maximize these tax-advantaged vehicles.

Pre-Approval: Do not shop without one. A mortgage pre-approval locks in a rate for a set period, protecting you from sudden market hikes while you search.

2. The Roadmap for Mortgage Renewals

If your mortgage term expires in 2026, you might be anxious about interest rates. This is known as the "renewal cliff," but with Mortgage Architects Bennett Capital, it’s just another bridge we help you cross.

Do not simply sign the renewal letter from your bank. Banks often offer existing clients higher rates, banking on the fact that you won't shop around. As a broker, we access mortgage renewal options from over 50 lenders to ensure you get a competitive product.

3. The Roadmap for Debt Consolidation & Refinancing

High-interest consumer debt (credit cards, lines of credit) can erode your financial stability. If you have built equity in your home, 2026 might be the year to restructure.

Mortgage refinancing allows you to roll high-interest debt into your lower-interest mortgage payment. This can significantly reduce your total monthly cash outflow, freeing up budget for savings or investments.

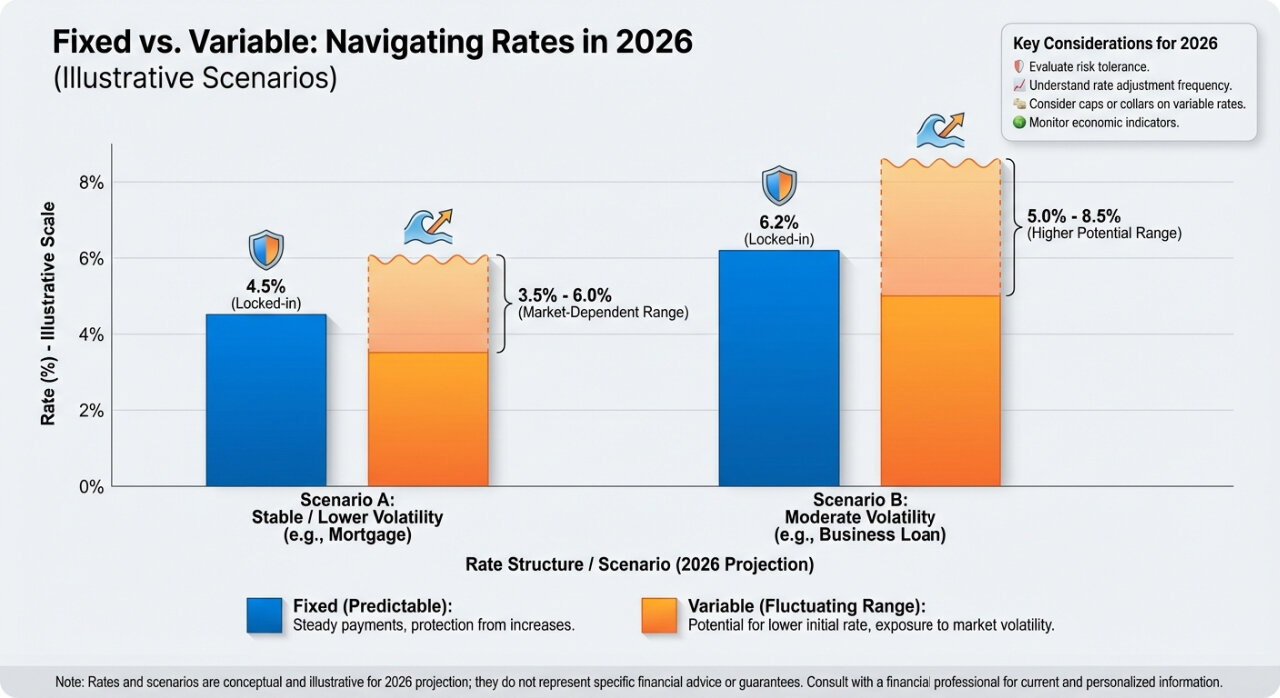

One of the most common questions we receive at our Kitchener office is: "Should I go fixed or variable?" The answer depends on your risk tolerance and the economic forecast. Here is a comparison to help you weigh your options.

Feature Fixed Rate Mortgage Variable Rate Mortgage Payment Stability High. Your interest rate and payment amount remain exactly the same for the entire term (e.g., 5 years). Low to Moderate. Your payment may fluctuate, or the portion going toward principal may change as prime rates move. Risk Profile Best for those who sleep better knowing exactly what their budget is. Protects you if rates skyrocket. Best for those with financial flexibility who believe rates will decrease. Potential to save money if the Bank of Canada cuts rates. Penalty for

Breaking Higher. Calculated using the Interest Rate Differential (IRD), which can be costly. Lower. Typically just three months' interest. 2026 Strategy Ideal if you believe rates have hit a bottom or want security during volatile times. Ideal if economists forecast a downward trend in rates throughout 2026.

Note: This table is for educational purposes. Always consult with Tracy Bennett to discuss your specific situation.

In a digital world, it is easy to treat a mortgage like a transaction. But a mortgage is tied to your home, your family, and your future. That is why working with a local Kitchener Mortgage Broker is distinct from using an algorithm or a big bank.

Tracy Bennett, our Lead Planner, often says, "My superpower is my empathy, my gift is getting to use it every day in the Mortgage Industry."

Why choose Bennett Capital Group from Mortgage Architects for your 2026 planning?

Access to 50+ Lenders: We don't push one bank's products. We shop the market for you, including major banks, credit unions, and monoline lenders.

Specialized Programs: From Self-Employed solutions to New to Canada programs, we have access to products that traditional branches often decline.

Long-Term Partnership: We don't just close the deal and disappear. We offer annual reviews to ensure your mortgage is still performing for you.

Pull Your Credit Report: Review it for errors. If your score needs work, let's start a credit repair plan today.

Calculate Your Equity: Understanding your loan-to-value ratio is essential for refinancing or purchasing investment property.

Review Your Budget: Has your income or spending changed? Update your budget to see what mortgage payment is comfortable, not just what is "approvable."

Book a Consultation: Don't wait until your renewal letter arrives. Contact us early to lock in rates and explore options.

1. How early should I start planning for my mortgage renewal in 2026?

We recommend starting the conversation 4 to 6 months before your maturity date. This allows us to secure a rate hold (typically 120 days) to protect you from potential rate increases while we compare lenders to find you the best deal. Starting early also gives you time to improve your credit score if necessary.

2. Can a mortgage broker in Kitchener get better rates than my bank?

Yes, in many cases. Because a mortgage broker like Mortgage Architects Bennett Capital Group sends millions of dollars in volume to various lenders, we often access "bulk rates" that are lower than advertised posted rates. Furthermore, we can negotiate on your behalf, whereas a bank representative is restricted to their specific institution's products.

3. I am self-employed. Will it be harder for me to get a mortgage in 2026?

Self-employed borrowers often face stricter scrutiny from traditional banks, but it is not impossible. We have access to lenders who specialize in self-employed mortgages. These lenders may look at your business cash flow or bank statements rather than just your T4s to approve your loan.

4. What is the stress test, and will it still apply in 2026?

The mortgage stress test requires borrowers to qualify at a rate higher than their actual contract rate (typically the contract rate plus 2% or the benchmark rate of 5.25%, whichever is higher). As of now, the stress test remains a federal requirement. It ensures you can afford your home if rates rise. We factor this into all our pre-approvals to ensure you are shopping within a realistic budget.

5. What if I want to buy a home that needs renovations?

We offer a Purchase Plus Improvement mortgage. This allows you to borrow the money for the purchase and the renovations in one mortgage. It is an excellent strategy for 2026 buyers looking at older homes in established Kitchener neighborhoods that need a modern touch.

2026 holds immense potential for homeowners and buyers in the Kitchener-Waterloo area. Whether the market fluctuates up or down, the stability of your financial future rests on the quality of advice you receive today. At Mortgage Architects Bennett Capital Group, our mission is to match you with products that suit your needs, serving you with integrity, respect, and experience.

Don't leave your largest financial asset to chance. Let's build your roadmap together.

Contact Tracy Bennett and the team at Mortgage Architects Bennett Capital Group today. Whether you are a first-time buyer or looking to renew, we are here to help you make your mortgage work for you.

Call: 519-576-4869

Email: [email protected]

Visit: www.bennettcapital.ca