If you are planning to enter the real estate market, you are likely wondering how much cash you actually need upfront. As a leading mortgage broker in Kitchener, ON, we hear this question daily. The rules and market dynamics have shifted heading into 2026, making it essential to understand your down payment options.

Many prospective buyers believe they need a massive twenty percent saved to purchase a property. Fortunately, that is a myth. Bennett Capital Group is here to help you navigate the nuances of securing a mortgage, ensuring you keep more money in your pocket while achieving your homeownership dreams.

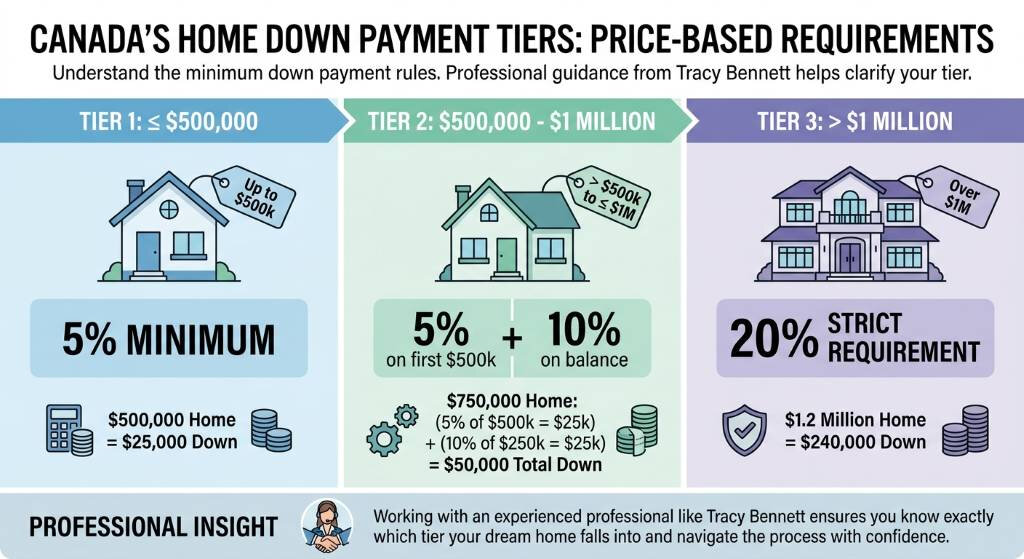

In Canada, the amount you need to put down is directly tied to the purchase price of the home. Working with an experienced professional like Tracy Bennett ensures you know exactly which tier your dream home falls into.

For homes priced at $500,000 or less, the minimum requirement is just 5%. If the home is between $500,000 and $1 million, you will need 5% for the first $500,000 and 10% for the remaining balance. For properties over $1 million, a strict 20% is required. Keep in mind that any down payment under 20% means you will need mortgage default insurance, often referred to as CMHC insurance.

Let us look at how this translates into real numbers for the Kitchener real estate market.

| Home Purchase Price | Down Payment Calculation | Minimum Down Payment Required |

|---|---|---|

| $400,000 | 5% of $400,000 | $20,000 |

| $650,000 | 5% of $500k + 10% of $150k | $40,000 |

| $850,000 | 5% of $500k + 10% of $350k | $60,000 |

| $1,100,000 | 20% of $1,100,000 | $220,000 |

Saving up tens of thousands of dollars is no small feat. Thankfully, 2026 brings continued support through various government programs and alternative funding sources. As your dedicated Kitchener mortgage experts, we can help you explore all available avenues.

By combining these strategies, you can reach your goal much faster than relying on traditional savings alone.

Q1: Can I buy a home in Kitchener with zero down payment?

No, traditional zero-down mortgages are no longer available in Canada. However, you can use borrowed funds like a line of credit for your down payment in some specific flex-down programs, provided you have excellent credit.

Q2: What is the First Home Savings Account (FHSA)?

The FHSA is a registered plan allowing prospective first-time home buyers to save up to $40,000 tax-free. Contributions are tax-deductible, and withdrawals to purchase a qualifying home are non-taxable.

Q3: Does my down payment affect my mortgage rate?

Yes, it can. Mortgages with less than a 20% down payment are insured, which lowers the risk for the lender. As a result, insured mortgages often come with slightly lower interest rates compared to uninsured mortgages.

Q4: Can I use a personal loan for my down payment?

It is possible through a borrowed down payment program, but the loan payments will be factored into your debt service ratios. This can significantly reduce the total mortgage amount you qualify for.

Q5: How do I get started with Mortgage Architects Bennett Capital Group?

Simply reach out to Tracy Bennett. We will review your financial situation, discuss your homeownership goals, and create a customized mortgage strategy to get you pre-approved.