If you are planning to enter the real estate market, you are likely wondering how much cash you actually need upfront. As a leading mortgage broker in Kitchener, ON, we hear this question daily. The rules and market dynamics have shifted heading into 2026, making it essential to understand your down payment options.

Many prospective buyers believe they need a massive twenty percent saved to purchase a property. Fortunately, that is a myth. Bennett Capital Group is here to help you navigate the nuances of securing a mortgage, ensuring you keep more money in your pocket while achieving your homeownership dreams.

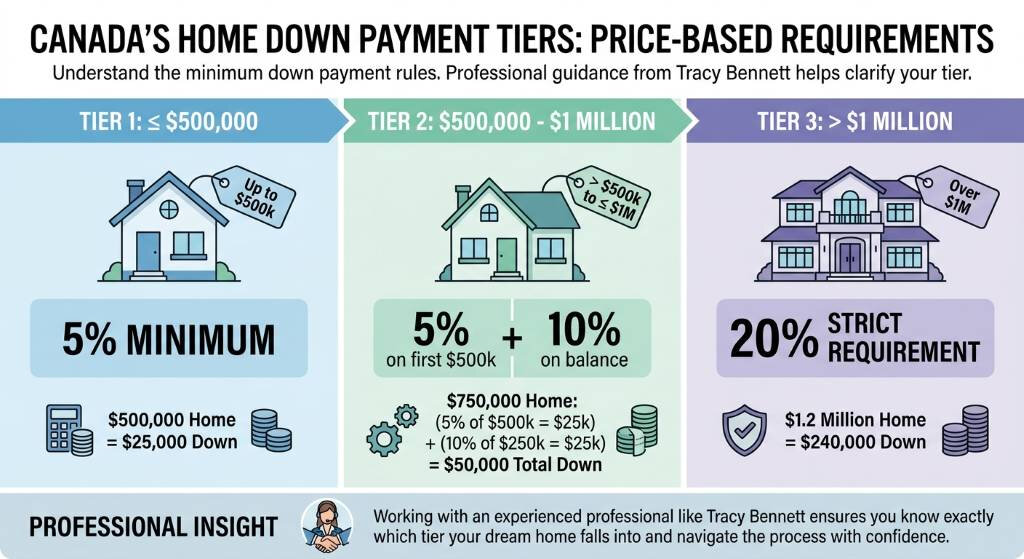

In Canada, the amount you need to put down is directly tied to the purchase price of the home. Working with an experienced professional like Tracy Bennett ensures you know exactly which tier your dream home falls into.

For homes priced at $500,000 or less, the minimum requirement is just 5%. If the home is between $500,000 and $1 million, you will need 5% for the first $500,000 and 10% for the remaining balance. For properties over $1 million, a strict 20% is required. Keep in mind that any down payment under 20% means you will need mortgage default insurance, often referred to as CMHC insurance.

Let us look at how this translates into real numbers for the Kitchener real estate market.

| Home Purchase Price | Down Payment Calculation | Minimum Down Payment Required |

|---|---|---|

| $400,000 | 5% of $400,000 | $20,000 |

| $650,000 | 5% of $500k + 10% of $150k | $40,000 |

| $850,000 | 5% of $500k + 10% of $350k | $60,000 |

| $1,100,000 | 20% of $1,100,000 | $220,000 |

Saving up tens of thousands of dollars is no small feat. Thankfully, 2026 brings continued support through various government programs and alternative funding sources. As your dedicated Kitchener mortgage experts, we can help you explore all available avenues.

By combining these strategies, you can reach your goal much faster than relying on traditional savings alone.

Q1: Can I buy a home in Kitchener with zero down payment?

No, traditional zero-down mortgages are no longer available in Canada. However, you can use borrowed funds like a line of credit for your down payment in some specific flex-down programs, provided you have excellent credit.

Q2: What is the First Home Savings Account (FHSA)?

The FHSA is a registered plan allowing prospective first-time home buyers to save up to $40,000 tax-free. Contributions are tax-deductible, and withdrawals to purchase a qualifying home are non-taxable.

Q3: Does my down payment affect my mortgage rate?

Yes, it can. Mortgages with less than a 20% down payment are insured, which lowers the risk for the lender. As a result, insured mortgages often come with slightly lower interest rates compared to uninsured mortgages.

Q4: Can I use a personal loan for my down payment?

It is possible through a borrowed down payment program, but the loan payments will be factored into your debt service ratios. This can significantly reduce the total mortgage amount you qualify for.

Q5: How do I get started with Mortgage Architects Bennett Capital Group?

Simply reach out to Tracy Bennett. We will review your financial situation, discuss your homeownership goals, and create a customized mortgage strategy to get you pre-approved.

As we approach the spring season, prospective homeowners and investors are keeping a close eye on the Kitchener housing market. The Spring 2026 housing market outlook for Kitchener, ON reveals exciting opportunities for buyers prepared to act. Working with a dedicated mortgage broker in Kitchener is more critical than ever to secure favorable rates and navigate fluctuating inventory levels.

Kitchener continues to attract families and young professionals due to its vibrant tech sector and excellent quality of life. If you are planning to purchase a home this year, understanding the local economic drivers and interest rate forecasts will give you a significant advantage. Our team at Bennett Capital Group is here to help you build a solid financial strategy.

Several unique factors are influencing property values and buyer competition in the Waterloo Region this year. Buyers must stay informed to make the best possible investment. Here are the top trends to watch:

By partnering with a trusted Kitchener mortgage professional, you can ensure your financing aligns perfectly with these emerging market realities.

| Property Type | Average Price (Projected Spring 2026) | Year-Over-Year Change | Average Days on Market |

|---|---|---|---|

| Detached Home | $895,000 | +3.2% | 18 Days |

| Townhouse | $680,000 | +2.5% | 14 Days |

| Condominium | $510,000 | +1.8% | 22 Days |

Preparation is the ultimate key to success in the Spring 2026 housing market. The first step every buyer should take is obtaining a rock-solid mortgage pre-approval. This not only dictates your budget but also signals to sellers that you are a serious, qualified buyer.

Expert Advice: Do not wait for the spring rush to hit its peak. Start organizing your financial documents, including income verification and tax returns, right now. Reach out to Bennett Capital Group to review your credit profile and explore all available mortgage products tailored to the Ontario market.

Please note that mortgage rates and lending guidelines are subject to change based on market conditions and individual qualifications. Always consult with a licensed mortgage broker to receive personalized advice suited to your specific financial situation.

Q1: Is Spring 2026 a good time to buy a home in Kitchener?

Yes, with stabilizing interest rates and an increase in housing inventory, Spring 2026 presents a balanced market for buyers looking to settle in the Kitchener area.

Q2: How much down payment do I need for a home in Ontario?

The minimum down payment is 5% for the first $500,000 of the purchase price and 10% for the portion between $500,000 and $999,999. Homes priced at $1 million or more require a minimum 20% down payment.

Q3: Why should I use a mortgage broker instead of a bank?

A mortgage broker like Tracy Bennett shops around with multiple lenders to find you the best rates and terms, saving you time and potentially thousands of dollars over the life of your mortgage.

Q4: What are closing costs, and how much should I budget for them?

Closing costs include land transfer taxes, legal fees, and appraisal fees. Buyers in Kitchener should typically budget between 1.5% and 4% of the purchase price to cover these expenses.

Q5: How long does a mortgage pre-approval last?

Most mortgage pre-approvals are valid for 90 to 120 days. This gives you a secure rate guarantee while you shop for your new home during the spring market.

Navigating the Kitchener-Waterloo Real Estate Market with Confidence

Entering the real estate market in 2026 requires more than just a wish list and a down payment; it requires a strategic financial foundation. In the bustling Kitchener-Waterloo (KWC) region, inventory moves quickly, and sellers prioritize buyers who can prove they are serious. This is where a mortgage pre-approval becomes your most valuable tool.

At Mortgage Architects Bennett Capital Group, we have seen firsthand how the landscape has shifted. Whether you are securing a first-time home buyer mortgage , struggling to find a detached home within budget, or looking to refinance your current property, securing a pre-approval is the first critical step. It does more than just tell you what you can afford; it locks in your mortgage rates for a specific period (typically 90 to 120 days), shielding you from potential rate hikes driven by shifting bond yields mortgage rates while you shop.

Tracy Bennett and our team of experts access over 50 lenders, including the best mortgage lenders in Ontario, to tailor a solution that fits your specific financial picture, ensuring you are ready to make a firm offer when the right property appears.

The Strategic Advantages of Early Pre-Approval

Why is getting approved early so critical in the 2026 market? It comes down to leverage and clarity. When you work with a top mortgage broker Kitchener Waterloo like Bennett Capital Group from Mortgage Architects, you gain a clear understanding of your maximum purchase price, monthly payments, and down payment requirements.

Rate Protection: In a fluctuating economic environment, a pre-approval holds today's best rates for you. If rates drop, you get the lower rate; if they rise, you are protected.

Budget Certainty: Avoid the heartbreak of falling in love with a home you can't afford. Many buyers face stiff competition; knowing your exact hard cap prevents over-bidding.

Seller Confidence: In multiple-offer situations, understanding the difference between a pre-qualified vs. pre-approved mortgage is vital. A buyer with a fully verified pre-approval letter is viewed as a 'sure thing' compared to someone who only has a basic mortgage pre-qualification.

Our team also specializes in complex scenarios, including securing home loans for those new to Canada and facilitating standard conventional loans, ensuring every buyer has a fair shot at homeownership.

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Data Verification | Based on verbal info (Self-reported) | Based on verified documents (Income, Credit) |

| Credit Check | Soft check or none | Hard credit inquiry |

| Rate Hold | Rarely included | Yes (typically 90-120 days) |

| Competitive Edge | Low | High (Preferred by Sellers) |

How to Secure Your Pre-Approval with Mortgage Architects Bennett Capital Group

Ready to start your journey? The process is straightforward when you have the right guidance. To get your mortgage pre-approval online or in-person, you will need to provide proof of income (pay stubs, T4s, or NOAs), proof of down payment, and consent for a credit check. Once we review your financial profile, we can determine your exact borrowing power with local Ontario mortgage lenders.

Important Compliance Note: A pre-approval is a conditional commitment from a lender. It is subject to the property meeting the lender's criteria and your financial situation remaining stable before closing. It is also important to consider how the new mortgage rules Dec 15 may impact your qualifying rate. Always consult with your mortgage broker before making significant financial changes.

Don't navigate the 2026 housing market alone. Contact Mortgage Architects Bennett Capital Group at (519) 576-4869 to discuss your options.

Q1: What is a mortgage pre-approval vs. pre-qualification?

A pre-qualification is a quick estimate based on unverified information. A pre-approval is a conditional commitment from a lender after thoroughly verifying your income, credit, and assets, giving you a concrete budget and a guaranteed rate hold.

Q2: How long is a mortgage pre-approval valid for in 2026?

Typically, a pre-approval locks in your interest rate for 90 to 120 days, giving you ample time to shop for a home in the KWC area without worrying about rate hikes.

Q3: Does getting pre-approved hurt my credit score?

A pre-approval requires a hard inquiry on your credit report, which may cause a temporary, minor dip in your score. However, this is necessary to secure a mortgage and shows sellers you are a serious buyer.

Q4: What is the minimum down payment required in Kitchener?

For homes under $500,000, the minimum is 5%. For homes between $500,000 and $1 million, it is 5% on the first $500k and 10% on the remainder. Keep in mind, any down payment under 20% creates a high-ratio mortgage and requires default insurance (such as CMHC mortgages). We highly recommend using a closing costs in Ontario calculator to estimate your total cash required on closing day.

Q5: Can I get pre-approved if I am self-employed?

Yes! Mortgage Architects Bennett Capital Group specializes in self-employed mortgages. We can help you navigate alternative documentation or secure a stated income mortgage to prove your income stability. We also assist business owners with commercial needs, including capital lease financing and capital equipment leasing.

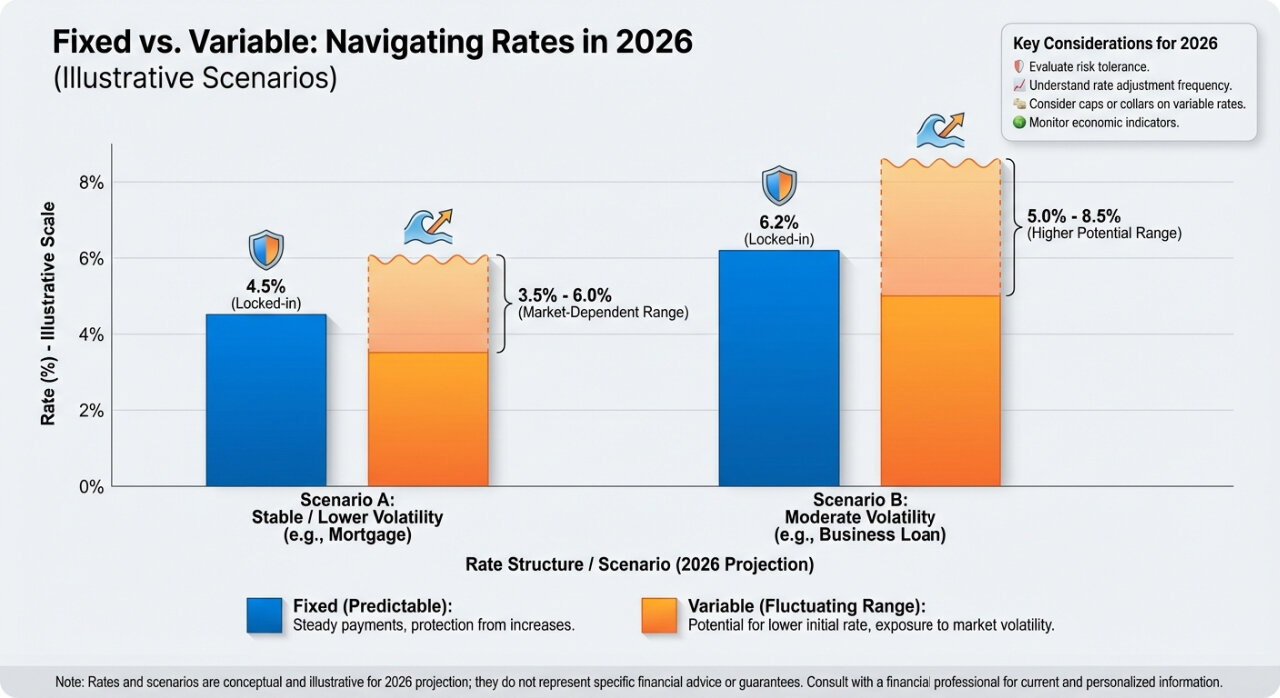

One of the most persistent debates in the mortgage world is the choice between fixed and variable rates. In Q1 2026, this decision carries new weight. Over the past year, we have observed a narrowing gap between these two options. Historically, variable rates offered immediate savings with the risk of fluctuation, while fixed rates provided security at a premium. Today, the spread has adjusted, requiring buyers to look closely at their long-term financial goals and risk tolerance.

For buyers in the Tri-Cities area, where property values—especially for detached homes—remain robust, the stability of a fixed rate can offer peace of mind. Knowing exactly what your principal and interest payments will be for the next three to five years allows for precise budgeting. This is particularly beneficial for young families or those entering the market with a tighter debt-to-income ratio. On the other hand, seasoned investors or those with higher cash flow flexibility might still find value in variable products, betting on potential rate decreases later in the year.

It is also essential to consider Mortgage Pre-Approval before you start shopping. A pre-approval in 2026 does more than just hold a rate; it demonstrates to sellers that you are a serious buyer in a competitive market. At Bennett Capital, we help you analyze these options using our Mortgage Calculator to simulate different scenarios. We look at the "what ifs"—what if rates drop? What if they rise? By stress-testing your budget against current Q1 2026 rates, we ensure that your dream home doesn't become a financial burden.

| Mortgage Strategy | Ideal Candidate Profile | Key Benefit in Q1 2026 | Risk Factor |

|---|---|---|---|

| 5-Year Fixed Rate | First-time buyers, families on a strict budget. | Maximum stability; immunity to rate hikes during the term. | Potential penalty if breaking the mortgage early; less flexibility if rates drop significantly. |

| Variable Rate | Investors, buyers with disposable income buffer. | Potential to pay less interest if the prime rate decreases. | Monthly payments or amortization periods may increase if the prime rate rises. |

| Short-Term Fixed (1-3 Years) | Homeowners planning to move soon or expecting rate drops. | Balance of stability and flexibility to renegotiate sooner. | Renewal risk in the near future if rates spike unexpectedly. |

| Hybrid Mortgage | Conservative borrowers wanting to hedge bets. | Diversifies risk by splitting the mortgage between fixed and variable portions. | More complex to manage; may limit switching lenders easily. |

Mortgage Renewals and Refinancing Opportunities for Existing Homeowners

If you purchased your home around 2021, you are likely approaching your maturity date. Mortgage renewals in 2026 are a hot topic because the rates today are different from the historic lows seen five years ago. Many homeowners fear the "payment shock" associated with renewing at a higher rate. However, simply signing the renewal letter from your current bank is rarely the best strategy. Banks often offer posted rates that are not their most competitive. By working with a broker like Bennett Capital Group, you can shop the market to find lenders competing for your business.

Furthermore, Q1 2026 presents excellent opportunities for Mortgage Refinancing. Homeowners in Kitchener and Waterloo have seen significant appreciation in property values over the last half-decade. This accumulated equity can be leveraged to consolidate high-interest debt, such as credit cards or lines of credit, into a single, lower mortgage interest rate. This strategy can significantly improve monthly cash flow, even if the mortgage rate itself is higher than your previous term.

Another avenue to explore is the "Purchase Plus Improvement" program or refinancing for renovations. If you love your location but need to update your home, using your equity to fund renovations is often cheaper than selling and buying a new property. Whether it is adding a suite for income potential or modernizing a kitchen, refinancing allows you to reinvest in your asset. We also specialize in helping Self-Employed individuals and those going through life transitions like separation or divorce to restructure their financing in a way that supports their new reality.

Q1: What are the predicted mortgage rate trends for the remainder of 2026?

While no one can predict the market with 100% certainty, economic indicators in Q1 2026 suggest a period of stabilization. Most analysts do not foresee the aggressive rate hikes of previous years, but significant drops are also unlikely in the immediate term. The market is favoring a "higher for longer" baseline compared to pre-2020, meaning buyers should budget for current rates rather than waiting for a drastic crash.

Q2: How does a mortgage broker in Kitchener get better rates than my bank?

A mortgage broker has access to the "wholesale" mortgage market. While a bank creates its own products, a broker like Bennett Capital Group negotiates with over 50 different lenders, including major banks, credit unions, and monoline lenders. This volume allows us to access rate discounts and proprietary products that are not available to the general public walking into a bank branch.

Q3: Is it harder to qualify for a mortgage in 2026 compared to previous years?

Qualification standards, including the stress test, remain stringent to ensure borrower stability. However, lenders have introduced more innovative programs for niche borrowers, such as new Canadians and self-employed individuals. While the "stress test" rate (qualifying rate) is still applicable, working with a broker can help you find lenders with more flexible debt-service ratios or alternative income verification methods.

Q4: I want to buy a home in Waterloo but have a small down payment. What are my options?

For homes under $500,000, the minimum down payment is 5%. For homes between $500,000 and $999,999, it is 5% on the first $500k and 10% on the remainder. If you have less than a 20% down payment, you will need mortgage default insurance (often called CMHC insurance). We can help you navigate these tiers and even explore first-time home buyer incentives that may be available to assist with your down payment.

Q5: When should I start the mortgage renewal process?

You should start the conversation at least 4 to 6 months before your maturity date. This allows us to lock in a rate for you well in advance. If rates drop before your renewal date, we can usually adjust to the lower rate, but if they rise, you are protected by the rate hold. Waiting until the last minute limits your options and negotiating power.

Book Your Free Mortgage Consultation with Tracy Bennett Today

If the last few years have taught us anything in the world of real estate and finance, it is that preparation is power. As we look toward the horizon of 2026, homeowners and prospective buyers in Kitchener-Waterloo face a unique economic landscape. Whether you are looking to purchase your first home, renewing a mortgage that was locked in during the low-rate era, or considering leveraging equity for investment, having a strategic plan is non-negotiable.

At Mortgage Architects Bennett Capital Group, we believe that your mortgage should work for you, not the other way around. Led by Tracy Bennett, a veteran mortgage planner with over 35 years of experience, our team creates personalized roadmaps that account for market shifts, interest rate forecasts, and your personal financial goals. Here is your comprehensive guide to mortgage planning for 2026.

The year 2026 is shaping up to be a significant milestone for the Canadian housing market. Many mortgages originated during the peak of the housing boom (2020-2021) will be coming up for renewal. For many residents in the Waterloo Region, this means transitioning from historically low interest rates to a new financial reality.

However, it isn't all challenges. Markets are cyclical. By planning now, you can mitigate "payment shock," take advantage of potential rate stabilizations, and position yourself to build wealth. A proactive approach involves reviewing your current financial health, understanding the local Kitchener real estate market, and consulting with a trusted mortgage broker well before your maturity date.

Real estate is hyper-local. While national headlines give a broad overview, the dynamics in Kitchener, Waterloo, and Cambridge are distinct. Our region remains a hub for technology, education, and manufacturing, driving consistent demand for housing.

Inventory Levels: We anticipate a balanced market in 2026, offering more negotiation power for buyers than in previous frenzied years.

Population Growth: With new Canadians and young professionals moving to the Tri-Cities, competition for entry-level homes and rentals remains steady.

Property Values: While prices have stabilized, long-term equity growth in Kitchener remains a strong bet for wealth accumulation.

Whether you are looking at a condo in downtown Kitchener or a detached home in the suburbs, understanding these local nuances is part of our service at Bennett Capital Group from Mortgage Architects. We don't just find you a rate; we help you find a home strategy.

One size does not fit all. Your roadmap for 2026 depends entirely on your current position on the property ladder.

1. The Roadmap for First-Time Home Buyers

If 2026 is the year you plan to stop renting and start owning, you need to start preparing 6 to 12 months in advance. The "dream of homeownership" requires concrete financial steps.

Credit Consulting: A strong credit score is your ticket to the best rates. We offer credit consulting to help you polish your report before lenders see it.

Down Payment Strategy: Are you utilizing the First Home Savings Account (FHSA) or the Home Buyers' Plan (HBP)? We can guide you on how to maximize these tax-advantaged vehicles.

Pre-Approval: Do not shop without one. A mortgage pre-approval locks in a rate for a set period, protecting you from sudden market hikes while you search.

2. The Roadmap for Mortgage Renewals

If your mortgage term expires in 2026, you might be anxious about interest rates. This is known as the "renewal cliff," but with Mortgage Architects Bennett Capital, it’s just another bridge we help you cross.

Do not simply sign the renewal letter from your bank. Banks often offer existing clients higher rates, banking on the fact that you won't shop around. As a broker, we access mortgage renewal options from over 50 lenders to ensure you get a competitive product.

3. The Roadmap for Debt Consolidation & Refinancing

High-interest consumer debt (credit cards, lines of credit) can erode your financial stability. If you have built equity in your home, 2026 might be the year to restructure.

Mortgage refinancing allows you to roll high-interest debt into your lower-interest mortgage payment. This can significantly reduce your total monthly cash outflow, freeing up budget for savings or investments.

One of the most common questions we receive at our Kitchener office is: "Should I go fixed or variable?" The answer depends on your risk tolerance and the economic forecast. Here is a comparison to help you weigh your options.

Feature Fixed Rate Mortgage Variable Rate Mortgage Payment Stability High. Your interest rate and payment amount remain exactly the same for the entire term (e.g., 5 years). Low to Moderate. Your payment may fluctuate, or the portion going toward principal may change as prime rates move. Risk Profile Best for those who sleep better knowing exactly what their budget is. Protects you if rates skyrocket. Best for those with financial flexibility who believe rates will decrease. Potential to save money if the Bank of Canada cuts rates. Penalty for

Breaking Higher. Calculated using the Interest Rate Differential (IRD), which can be costly. Lower. Typically just three months' interest. 2026 Strategy Ideal if you believe rates have hit a bottom or want security during volatile times. Ideal if economists forecast a downward trend in rates throughout 2026.

Note: This table is for educational purposes. Always consult with Tracy Bennett to discuss your specific situation.

In a digital world, it is easy to treat a mortgage like a transaction. But a mortgage is tied to your home, your family, and your future. That is why working with a local Kitchener Mortgage Broker is distinct from using an algorithm or a big bank.

Tracy Bennett, our Lead Planner, often says, "My superpower is my empathy, my gift is getting to use it every day in the Mortgage Industry."

Why choose Bennett Capital Group from Mortgage Architects for your 2026 planning?

Access to 50+ Lenders: We don't push one bank's products. We shop the market for you, including major banks, credit unions, and monoline lenders.

Specialized Programs: From Self-Employed solutions to New to Canada programs, we have access to products that traditional branches often decline.

Long-Term Partnership: We don't just close the deal and disappear. We offer annual reviews to ensure your mortgage is still performing for you.

Pull Your Credit Report: Review it for errors. If your score needs work, let's start a credit repair plan today.

Calculate Your Equity: Understanding your loan-to-value ratio is essential for refinancing or purchasing investment property.

Review Your Budget: Has your income or spending changed? Update your budget to see what mortgage payment is comfortable, not just what is "approvable."

Book a Consultation: Don't wait until your renewal letter arrives. Contact us early to lock in rates and explore options.

1. How early should I start planning for my mortgage renewal in 2026?

We recommend starting the conversation 4 to 6 months before your maturity date. This allows us to secure a rate hold (typically 120 days) to protect you from potential rate increases while we compare lenders to find you the best deal. Starting early also gives you time to improve your credit score if necessary.

2. Can a mortgage broker in Kitchener get better rates than my bank?

Yes, in many cases. Because a mortgage broker like Mortgage Architects Bennett Capital Group sends millions of dollars in volume to various lenders, we often access "bulk rates" that are lower than advertised posted rates. Furthermore, we can negotiate on your behalf, whereas a bank representative is restricted to their specific institution's products.

3. I am self-employed. Will it be harder for me to get a mortgage in 2026?

Self-employed borrowers often face stricter scrutiny from traditional banks, but it is not impossible. We have access to lenders who specialize in self-employed mortgages. These lenders may look at your business cash flow or bank statements rather than just your T4s to approve your loan.

4. What is the stress test, and will it still apply in 2026?

The mortgage stress test requires borrowers to qualify at a rate higher than their actual contract rate (typically the contract rate plus 2% or the benchmark rate of 5.25%, whichever is higher). As of now, the stress test remains a federal requirement. It ensures you can afford your home if rates rise. We factor this into all our pre-approvals to ensure you are shopping within a realistic budget.

5. What if I want to buy a home that needs renovations?

We offer a Purchase Plus Improvement mortgage. This allows you to borrow the money for the purchase and the renovations in one mortgage. It is an excellent strategy for 2026 buyers looking at older homes in established Kitchener neighborhoods that need a modern touch.

2026 holds immense potential for homeowners and buyers in the Kitchener-Waterloo area. Whether the market fluctuates up or down, the stability of your financial future rests on the quality of advice you receive today. At Mortgage Architects Bennett Capital Group, our mission is to match you with products that suit your needs, serving you with integrity, respect, and experience.

Don't leave your largest financial asset to chance. Let's build your roadmap together.

Contact Tracy Bennett and the team at Mortgage Architects Bennett Capital Group today. Whether you are a first-time buyer or looking to renew, we are here to help you make your mortgage work for you.

Call: 519-576-4869

Email: [email protected]

Visit: www.bennettcapital.ca